Bank Transfer Vs Wire Transfer

Table of Contents

Author: Mehdi Punjwani

We only list companies that are trustworthy and appropriately licensed. Our aim is to give you a comprehensive view of the regulated money transfer marketplace.

DisclosureMoneyTransfers aims to help users find the best money transfer provider for their needs. To support our free service, we may earn a commission from some of the providers listed in our search results. The commission may also impact the ordering of the providers shown. Our reviews are independent from this and are based on our editorial policy, research and testing of dozens of remittance providers on the market.

Table of Contents

What is the Difference Between Bank Transfers and Wire Transfers?

The key differences between bank transfers and wire transfers are:

Bank transfers | Wire transfers | |

|---|---|---|

System(s) | Automated Clearing House (ACH) to clear and settle the amount | Society for Worldwide Interbank Financial Telecommunications (SWIFT) to communicate across international borders if required. Clearing House Interbank Payments Systems (CHIPS) or Fedwire to clear and settle the amount. |

Range | International and domestic | |

Speed | 1-3 days | International: 1-5 days Domestic: 0-5 days |

Cost | $10-$30 | International: $20-$50 Domestic: $10-$30 |

Purpose | Personal use, bill payments, payment method for international transfers through money transfer providers | Personal use, remittance, property purchase and other large transactions |

What is a Wire Transfer?

A wire transfer is a way of sending money electronically between two financial institutions, such as banks or money transfer providers. Wire transfers can be carried out internationally as well as domestically.

In the USA wire transfers are carried out in either one or two stages, depending on if it’s domestic or international.

International Wire Transfers first require two banks to communicate with each other through the SWIFT network to confirm the transfer details. They then send the money through an intermediary system or ‘clearing house’ so it can arrive at the destination

Domestic Wire Transfers do not require the first communication stage, so banks can immediately send money to be processed in the ‘clearing house’

What is a Clearing House?

A clearing house is an intermediary organization that is responsible for handling financial transactions such as money transfers or securities. They are designed to improve banking efficiency and reduce the risk of either sending or receiving parties falling short of requirements involved in a transaction.

The Automated Clearing House (ACH) is an example of such in the USA. The sending bank transfers money to the ACH, which processes multiple transfers a day and settles them by the end of each day. They ‘clear’ the transaction so both sending and receiving parties are happy with the details, and ‘settle’ it by moving the funds on to the recipient bank.

How Do SWIFT Transfers Work?

International money transfers require an extra step before the money is sent through a clearing house, which involves sending over details about the transaction between the banks involved. This takes place over the Society for Worldwide Interbank Financial Telecommunications (SWIFT) banking system.

The SWIFT banking system works as a messaging service and is crucial before the actual exchange can occur. As over 11,000 banks across the world are on the SWIFT system, it allows for them to communicate important transaction details to each other in order to facilitate international money transfers.

If Person A is in the UK and wants to send money to Person B in the USA, this is how SWIFT would help:

Person A Starts the Transfer

Person A informs Bank A that they want to send money to Person B’s bank account with Bank B

The Banks Communicate With Each Other

Bank A communicates directly with Bank B via the SWIFT banking system with instructions about the bank transfer - the sending bank account, the receiving bank account, and the exact amount to be transferred

The Money is Moved via a Clearing House

No money is transferred through the SWIFT system, just instructions. The money is moved separately through the first channel outlined above, either through CHIPS or Fedwire

How Do Wire Transfers Work?

Domestic and international wire transfers both work by using a middleman or ‘clearing house’ to actually move the money from one account to another. This makes up the second stage of the transfer.

For example, if Person A wants to send money from their bank account with Bank A to be received by Person B in their bank account with Bank B:

Person A starts the Transfer

Person A informs Bank A that they want to send money to Person B’s bank account with Bank B

Bank A Talks to Bank B Over SWIFT

For international transfers, Bank A will inform Bank B of the transaction details via the SWIFT system. For domestic transfers this is not required.

Bank A Sends Money to CHIPS/Fedwire

Bank A sends their money to the clearing house, either Fedwire or the Clearing House Interbank Payments Systems (CHIPS) in the USA

CHIPS/Fedwire ‘Clears’ the Transfer

The clearing house ‘clears’ the transfer by confirming details about the transaction between Bank A and Bank B

CHIPS/Fedwire ‘Settles’ the Payment

The clearing house ‘settles’ the payment to Bank B, who credits the money into the bank account of Person B

Person B Receives the Money

Person B can then withdraw the money

Wire transfers between US banks are usually used for large transactions like property purchases, rather than every-day transactions.

Fedwire vs CHIPS

Fedwire and CHIPS are both used in the USA as clearing houses to process wire transfers. They’re both equipped to deal with international and domestic wire transfers, but the differences between the two are:

Fedwire | CHIPS |

|---|---|

Publicly owned by the Federal Reserve Bank | Privately owned by Clearing House Payments Company LLC - many large banks in the US own this company |

Faster and more expensive | Slower and cheaper |

Used for critical transactions that require immediate processing | Used for less important transactions, processed at the end of each working day |

Real time gross transactions: If Bank A needs to send Bank B $50,000 and Bank B needs to send Bank A $30,000, Fedwire will complete each transaction separately. | Net transactions: If Bank A needs to send Bank B $50,000 and Bank B needs to send Bank A $30,000, CHIPS will only transfer $20,000 from Bank A to Bank B |

What is a Bank Transfer?

A bank transfer is a different way of sending money electronically, and only works domestically. They are carried out through the Automated Clearing House system in the USA, which works as a middleman between financial institutions.

How Do Bank Transfers Work?

While bank transfers and wire transfers can both be used domestically, bank transfers are a more common way of handling day to day payments. For example, if Person A wanted to make a bank transfer from their account with Bank A to Person B’s account with Bank B, they would do the following:

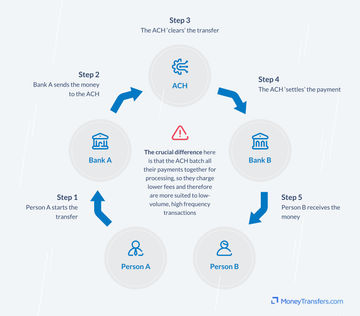

Person A Starts the Transfer

Person A would inform Bank A that they wanted to transfer a certain amount of money to Person B’s bank account

Bank A Sends the Money to the ACH

Bank A sends their money to the ACH, rather than CHIPS or Fedwire. The crucial difference here is that the ACH batch all their payments together for processing, so they charge lower fees and therefore are more suited to low-volume, high frequency transactions

The ACH ‘Clears’ the Transfer

The ACH ‘clears’ the transaction by confirming the details with Bank B

The ACH ‘Settles’ the Payment

The ACH ‘settles’ the payment to Bank B, who credits it into Person B’s account

Person B Receives the Money

Person B can then withdraw the money

Are There Free Alternatives to Bank Transfers?

As a result of the process above, bank transfers in the USA can be quite costly and time consuming. This is why many Americans use mobile wallets like Venmo, PayPal or Cash App for simple domestic money transactions - these companies use their own system to facilitate instant and free transfers between users.

Are Bank Transfers Expensive in Other Countries?

Bank transfers are not so costly in other countries. As a counter example, the ACH equivalent in the UK would be the Faster Payments System (FPS). A key distinction between the FPS and the ACH is that the FPS is free and instant, so people in the UK can and usually do use their banks to send money to each other.

They use mobile wallets like PayPal and Cash App too (Venmo isn’t available in the UK), but normally because they don’t have to use bank details to send money. Instead, with these apps they can just use an email, phone number or username.

How Do I Use a Bank Transfer to Send Money Internationally?

While bank transfers don’t let you send money internationally directly, you can use a bank transfer to pay for a money transfer provider to send money to a recipient in another country. If Person A was in the UK and wanted to send money to Person B in the USA, they would do the following:

The Transfer is Started

Person A makes a domestic bank transfer from their bank account with Bank A to the UK branch of a money transfer provider that allows transfers between the UK and USA, such as XE or WorldRemit

The Money Transfer Provider Organizes the Transfer

The money transfer provider issues instructions from their branch in the UK to their branch in the USA about the transfer, including details about the sender, the recipient and the exact amount being sent

The Transfer is Complete

The money transfer provider’s branch in the USA then gets the money to the recipient, either by sending it to their bank account, making it available as cash for collection, or depositing it into a mobile wallet

What’s important here is that the money doesn’t actually ever cross any international borders. The money transfer provider handles the whole transaction, and as they operate in multiple countries they can simply credit money from its branch in one country to its branch in another.

This means money transfer providers are able to avoid things like the SWIFT banking system and all the fees that come with it. It makes transferring money abroad easier, faster and cheaper.

Compare Money Transfer Providers

If you need to send money internationally, money transfer providers are the way to go for cheap, fast and simple transactions. Comparing providers with MoneyTransfers.com helps you find the best deal available for your transfer - just tell us how much you need to send and where it needs to go, and we’ll show you options from across the market.

You’ll be able to compare providers by the speed of your transfer, any fees you’ll pay, the exchange rate you’ll get, and the total amount of money the recipient will get at the end. Once you’ve found the deal you want, just click through to the provider and sign up in minutes, then you’ll be ready to send money abroad.

Can I send money between banks with a mobile app?

It is possible to send money between banks with a mobile app. However, it depends on if the bank offers this feature. You can check by searching for the banking app on Google Play and App Store. If you find the official banking app, then inspect the list of features to see if sending money is available.

Are bank transfers free?

The majority of bank transfers are not free. For example, wire transfers cost between $25 and $50. SEPA and domestic transfer can cost under $1, but they are limited to where you can send money. For free international transfers that come with minimal restrictions consider using a service like TorFX. Instead, they charge a currency exchange mark-up of around 1-3%.

Are instant bank transfers possible?

Most bank transfers take 1-5 business days, depending on the recipient's location and currencies involved. Bank transfers within the same network can be instant, such as SEPA transfers. However, for most international bank transfers expect to wait a few days.

Related Content

The Best International Money Transfer Companies

Using your bank for international wire transfers is expensive due to poor exchange rates and high fees.

Best Money Transfer Apps in India

Below, I’ll go over these in a bit more detail.

Transfer Money From Overseas to Australia: Tax Implications

In general, if you receive any income from abroad while in Australia and fall within the AU tax brackets, you will need to pay tax.

Sending Money Abroad

Ideal for sending money internationally, money transfer services have made huge strides in the past couple of decades to make sending your money abroad cheaper, faster, and easier than ever.

Send money with a debit card

Opting to send money online with a debit card is usually good for:

Contributors

Please share your experience with …